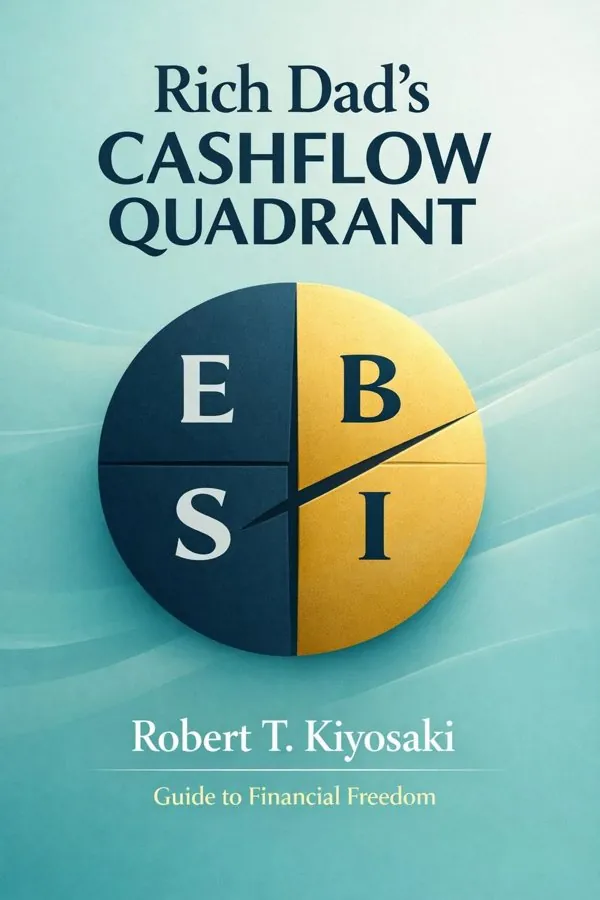

Rich Dad’s Cashflow Quadrant: Guide to Financial Freedom: Summary & Key Insights

Key Takeaways from Rich Dad’s Cashflow Quadrant: Guide to Financial Freedom

A person’s financial future is often shaped less by how much they earn than by how they earn it.

What most people call security is often just dependence in disguise.

Financial freedom usually begins when income stops depending entirely on personal labor.

Before people change their income sources, they usually need to change their identity.

Many people spend years chasing security without understanding the systems that shape money.

What Is Rich Dad’s Cashflow Quadrant: Guide to Financial Freedom About?

Rich Dad’s Cashflow Quadrant: Guide to Financial Freedom by Robert T. Kiyosaki is a finance book spanning 7 pages. Rich Dad’s Cashflow Quadrant is Robert T. Kiyosaki’s guide to understanding how people earn money, build wealth, and either remain trapped in financial dependency or move toward real freedom. The book introduces a simple but powerful framework: the four quadrants of income—Employee, Self-Employed, Business Owner, and Investor. Kiyosaki argues that most people spend their lives on the left side of the quadrant, where income depends heavily on personal effort, while lasting wealth is more often created on the right side, where systems and investments do the heavy lifting. What makes this book matter is not just its financial advice, but its insistence that wealth begins with a shift in thinking. Kiyosaki challenges conventional beliefs about job security, education, and retirement, urging readers to pursue financial education instead of relying on institutions for safety. Whether or not one agrees with every claim, the book has had enormous influence because it reframes money as a game of mindset, strategy, and structure. As an entrepreneur, investor, and author of the Rich Dad series, Kiyosaki writes with the authority of someone who has spent decades teaching people to think differently about income and independence.

This FizzRead summary covers all 8 key chapters of Rich Dad’s Cashflow Quadrant: Guide to Financial Freedom in approximately 10 minutes, distilling the most important ideas, arguments, and takeaways from Robert T. Kiyosaki's work. Also available as an audio summary and Key Quotes Podcast.

Rich Dad’s Cashflow Quadrant: Guide to Financial Freedom

Rich Dad’s Cashflow Quadrant is Robert T. Kiyosaki’s guide to understanding how people earn money, build wealth, and either remain trapped in financial dependency or move toward real freedom. The book introduces a simple but powerful framework: the four quadrants of income—Employee, Self-Employed, Business Owner, and Investor. Kiyosaki argues that most people spend their lives on the left side of the quadrant, where income depends heavily on personal effort, while lasting wealth is more often created on the right side, where systems and investments do the heavy lifting.

What makes this book matter is not just its financial advice, but its insistence that wealth begins with a shift in thinking. Kiyosaki challenges conventional beliefs about job security, education, and retirement, urging readers to pursue financial education instead of relying on institutions for safety. Whether or not one agrees with every claim, the book has had enormous influence because it reframes money as a game of mindset, strategy, and structure. As an entrepreneur, investor, and author of the Rich Dad series, Kiyosaki writes with the authority of someone who has spent decades teaching people to think differently about income and independence.

Who Should Read Rich Dad’s Cashflow Quadrant: Guide to Financial Freedom?

This book is perfect for anyone interested in finance and looking to gain actionable insights in a short read. Whether you're a student, professional, or lifelong learner, the key ideas from Rich Dad’s Cashflow Quadrant: Guide to Financial Freedom by Robert T. Kiyosaki will help you think differently.

- ✓Readers who enjoy finance and want practical takeaways

- ✓Professionals looking to apply new ideas to their work and life

- ✓Anyone who wants the core insights of Rich Dad’s Cashflow Quadrant: Guide to Financial Freedom in just 10 minutes

Want the full summary?

Get instant access to this book summary and 100K+ more with Fizz Moment.

Get Free SummaryAvailable on App Store • Free to download

Key Chapters

A person’s financial future is often shaped less by how much they earn than by how they earn it. That is the central insight behind the Cashflow Quadrant, a model that divides income earners into four groups: Employee (E), Self-Employed (S), Business Owner (B), and Investor (I). Employees work for a paycheck and value security, benefits, and predictable income. Self-employed people also work for money, but they prefer control and independence; they are specialists, freelancers, consultants, and small operators whose businesses often depend on their personal effort. On the other side, business owners create systems that can generate income without requiring their constant presence, while investors make money through assets such as businesses, real estate, stocks, or other investments.

Kiyosaki’s point is not that one quadrant is morally superior to another. Instead, each quadrant reflects a distinct mindset, set of values, and relationship to risk. An employee may prioritize stability, while an investor focuses on opportunity. A self-employed doctor may earn a high income, yet still be financially vulnerable if work stops. A business owner with a strong team and repeatable processes may have more freedom even with less day-to-day involvement.

This framework helps readers see why two people with similar incomes can have radically different levels of financial security. It also reveals why hard work alone does not always lead to wealth. Financial freedom depends on building assets and systems, not merely earning income.

Actionable takeaway: Identify which quadrant currently supplies most of your income, then ask which quadrant you want to move toward and what one skill you need to begin that shift.

What most people call security is often just dependence in disguise. Kiyosaki argues that the left side of the quadrant—Employees and Self-Employed individuals—is built on trading time for money. Employees exchange labor for wages, often believing that a steady job, promotions, and benefits will protect them. Self-employed people seek more control, but many of them simply create a job for themselves. If they stop working, the income often stops too.

This is not to say there is anything wrong with employment or independent work. Both can provide valuable experience, income, and satisfaction. The problem arises when people mistake earned income for financial freedom. A highly paid lawyer, dentist, or consultant may appear wealthy, but if their lifestyle depends on continued personal effort, their finances remain fragile. Illness, burnout, market changes, or industry disruption can quickly expose that vulnerability.

Kiyosaki wants readers to recognize that the left side often rewards effort but limits scale. There are only so many hours in a day, and personal capacity becomes the ceiling. Many self-employed people also struggle to delegate because they believe no one else can do the work as well as they can. That mindset keeps them busy, but not free.

A practical example is a freelancer who earns well but cannot take a month off without losing clients. Compare that to a company owner with a trained team and recurring revenue. The difference is not just income; it is structure. One person owns a job, while the other owns a system.

Actionable takeaway: If your income depends mainly on your presence, begin designing ways to separate earnings from hours worked through delegation, recurring revenue, or scalable services.

Financial freedom usually begins when income stops depending entirely on personal labor. That is why Kiyosaki places such importance on the right side of the quadrant: Business Owners and Investors. Business owners build organizations, processes, and teams that generate value even when they are not personally doing every task. Investors put money into assets that produce cash flow, appreciation, or both. In both cases, the goal is leverage.

Leverage means using systems, people, capital, and knowledge to multiply results. A business owner does not need to answer every email, serve every customer, or make every sale. Instead, they create a repeatable structure that others can operate. Likewise, an investor does not need to work another shift to earn more; a well-chosen asset can produce income over time. This is the shift from earning money to having money work for you.

Kiyosaki emphasizes that many people on the right side also take risks, but they take informed, structured risks. A restaurant owner with documented procedures, managers, and predictable operations has something far more valuable than a demanding job. An investor who studies markets, cash flow, and asset quality is not gambling blindly; they are allocating capital strategically.

For everyday readers, the lesson is not that everyone must immediately launch a large company or become a full-time investor. It is that wealth grows faster when you focus on ownership. Even small steps—buying dividend-producing assets, creating digital products, or building a business with staff rather than doing all the work yourself—move you toward the right side.

Actionable takeaway: Choose one asset or system you can start building this year that could produce income without requiring your constant direct labor.

Before people change their income sources, they usually need to change their identity. Kiyosaki insists that moving from the left side of the quadrant to the right side is not primarily a technical process; it is a psychological one. Employees often value certainty. Self-employed people value control and personal competence. Business owners and investors, by contrast, must become comfortable with delegation, uncertainty, and learning through mistakes.

This mindset shift is difficult because each quadrant rewards different beliefs. On the left side, success often means being reliable, skilled, and hardworking. On the right side, success requires thinking in terms of systems, assets, teams, and probabilities. Someone who says, “I need a stable salary before I can act,” may struggle to become an entrepreneur. Someone who says, “Only I can do this properly,” may never build a true business.

Kiyosaki also highlights the emotional barriers involved: fear of losing money, fear of criticism, and fear of failure. Many people remain in familiar patterns not because they are financially wise, but because they are emotionally comfortable. Yet growth demands the willingness to look inexperienced, make errors, and learn publicly.

A practical example is a talented consultant who wants to build an agency. The technical steps are important—hiring, pricing, systems—but the deeper challenge is trusting others to deliver work and accepting that imperfect delegation can still be more powerful than perfect personal control.

Actionable takeaway: Write down one belief about money or work that keeps you stuck—such as “security matters more than ownership” or “I must do everything myself”—and replace it with a more empowering principle you can test in action.

Many people spend years chasing security without understanding the systems that shape money. Kiyosaki argues that traditional education often trains people to become good workers, but not financially intelligent owners. Schools may teach academic skills and professional competence, yet leave people unprepared to understand taxes, assets, liabilities, leverage, cash flow, or risk. As a result, even high earners can remain financially fragile.

One of the book’s strongest claims is that job security is often an illusion. Companies restructure, industries change, and pensions disappear. A paycheck can feel safe, but if it is your only source of income, your safety rests in someone else’s hands. Financial education helps people recognize this dependence and begin building alternatives.

Kiyosaki encourages readers to learn the language of money. That means understanding the difference between income and cash flow, between owning a business and owning a job, between saving cash and acquiring productive assets. It also means examining how taxes, debt, and corporate structures affect wealth building. People who lack this knowledge may work hard for decades and still struggle, simply because they are following rules designed for employees rather than owners and investors.

A practical application is reviewing your finances not just by salary, but by asset growth. If your income rises but your expenses and liabilities rise with it, you may be moving faster without becoming freer. Financial intelligence helps you see beneath the surface.

Actionable takeaway: Commit to a personal financial education habit—such as reading one finance book a month, tracking your cash flow, or learning the basics of investing and tax structures.

Fear does not disappear when people pursue wealth; it simply changes form. Kiyosaki repeatedly emphasizes that one of the biggest differences between those who remain stuck and those who move toward financial freedom is their relationship with fear. Employees may fear losing a job. Self-employed people may fear losing clients or making mistakes. Aspiring business owners fear failure, debt, criticism, and uncertainty. Investors fear losing capital. The issue is not whether fear exists, but whether it becomes the decision-maker.

Kiyosaki does not present courage as recklessness. He is not telling readers to ignore risk or make impulsive financial moves. Instead, he suggests that fear should be managed through education, preparation, and gradual action. The unknown becomes less intimidating when it is studied. Risk becomes more tolerable when it is measured. Confidence grows when people move from passive anxiety to active learning.

A practical example is someone who wants to invest in real estate but is paralyzed by the possibility of loss. Rather than leaping blindly into a purchase, they could start by studying markets, analyzing deals, speaking with experienced investors, and reviewing cash flow models. Action reduces vague fear and replaces it with specific judgment.

Kiyosaki also reminds readers that fear of change often hides behind reasonable-sounding excuses. People say they are “waiting for the right time,” when in reality they are postponing discomfort. Financial freedom demands emotional resilience: the ability to act before certainty is available.

Actionable takeaway: Choose one financial fear you have been postponing—investing, selling, hiring, starting a business—and take the smallest concrete educational or practical step toward it this week.

The journey from the left side of the quadrant to the right side rarely happens overnight. Kiyosaki’s message is not that people should instantly quit their jobs or abandon stable income. Rather, the smart move is often to build the next quadrant while still supported by the current one. Financial freedom is usually created in stages, through deliberate transition rather than dramatic escape.

This idea matters because many readers assume wealth requires a radical leap. In reality, crossing over often begins with disciplined side efforts. An employee might use evening hours to learn sales, accounting, or investing. A self-employed designer might start documenting processes so work can be delegated. A professional with savings might begin acquiring small assets that produce income. Over time, these efforts can reduce dependence on earned income and increase ownership.

Kiyosaki places strong emphasis on skills that support the transition. Sales ability, communication, leadership, financial literacy, and risk assessment are all more important than credentials alone. People often focus too much on product knowledge and too little on business capability. A great technician may fail in business, while an average technician with strong systems and people skills can thrive.

A practical example is someone with a full-time job who starts a simple service business, hires part-time help, and reinvests profits into dividend funds or rental property. The first goal is not instant riches; it is to build alternative cash flow streams that gradually expand freedom.

Actionable takeaway: Map a 12-month transition plan that includes one income stream to build, one business or investing skill to learn, and one measurable target for reducing dependence on your primary paycheck.

A high income can improve comfort, but assets create freedom. This distinction runs through Kiyosaki’s philosophy. Many people assume that earning more automatically solves financial problems. Yet without asset accumulation, higher earnings can simply fund a more expensive lifestyle. Financial independence comes when your assets generate enough cash flow to cover your expenses, making work optional rather than compulsory.

In the Cashflow Quadrant framework, assets are anything that put money into your pocket consistently. Depending on the context, that may include rental properties, private businesses, dividend-producing investments, royalties, intellectual property, or ownership stakes in cash-flowing ventures. The emphasis is on productive ownership rather than consumption. A luxury car may signal success, but unless it creates income, it is not an asset in Kiyosaki’s terms.

This insight changes how readers evaluate financial decisions. Instead of asking, “Can I afford this?” a more powerful question becomes, “What asset will pay for this?” That shift encourages delayed gratification and strategic allocation of capital. It also exposes the trap of lifestyle inflation, where increased earnings disappear into larger homes, nicer vacations, and recurring expenses.

For example, someone receiving a bonus could spend it on status purchases or use it as seed capital for an asset that throws off recurring income. The first choice may feel rewarding today; the second builds long-term flexibility.

Actionable takeaway: Review your last six months of spending and identify how much went toward assets versus consumption, then set a target to direct a larger share of future income into cash-flow-producing ownership.

All Chapters in Rich Dad’s Cashflow Quadrant: Guide to Financial Freedom

About the Author

Robert T. Kiyosaki is an American entrepreneur, investor, speaker, and author best known for reshaping mainstream conversations about money through his Rich Dad series. He rose to international prominence with Rich Dad Poor Dad, a personal finance classic that contrasts traditional beliefs about work and security with a more entrepreneurial, asset-focused approach to wealth. Kiyosaki’s writing emphasizes financial education, business ownership, investing, real estate, and the importance of building cash-flow-producing assets. Over the years, he has become one of the most recognizable voices in personal finance, encouraging readers to question conventional advice about jobs, debt, school, and retirement. Though some of his ideas are debated, his influence is undeniable: he has inspired millions to think beyond salary and toward long-term financial independence.

Get This Summary in Your Preferred Format

Read or listen to the Rich Dad’s Cashflow Quadrant: Guide to Financial Freedom summary by Robert T. Kiyosaki anytime, anywhere. FizzRead offers multiple formats so you can learn on your terms — all free.

Available formats: App · Audio · PDF · EPUB — All included free with FizzRead

Download Rich Dad’s Cashflow Quadrant: Guide to Financial Freedom PDF and EPUB Summary

Key Quotes from Rich Dad’s Cashflow Quadrant: Guide to Financial Freedom

“A person’s financial future is often shaped less by how much they earn than by how they earn it.”

“What most people call security is often just dependence in disguise.”

“Financial freedom usually begins when income stops depending entirely on personal labor.”

“Before people change their income sources, they usually need to change their identity.”

“Many people spend years chasing security without understanding the systems that shape money.”

Frequently Asked Questions about Rich Dad’s Cashflow Quadrant: Guide to Financial Freedom

Rich Dad’s Cashflow Quadrant: Guide to Financial Freedom by Robert T. Kiyosaki is a finance book that explores key ideas across 8 chapters. Rich Dad’s Cashflow Quadrant is Robert T. Kiyosaki’s guide to understanding how people earn money, build wealth, and either remain trapped in financial dependency or move toward real freedom. The book introduces a simple but powerful framework: the four quadrants of income—Employee, Self-Employed, Business Owner, and Investor. Kiyosaki argues that most people spend their lives on the left side of the quadrant, where income depends heavily on personal effort, while lasting wealth is more often created on the right side, where systems and investments do the heavy lifting. What makes this book matter is not just its financial advice, but its insistence that wealth begins with a shift in thinking. Kiyosaki challenges conventional beliefs about job security, education, and retirement, urging readers to pursue financial education instead of relying on institutions for safety. Whether or not one agrees with every claim, the book has had enormous influence because it reframes money as a game of mindset, strategy, and structure. As an entrepreneur, investor, and author of the Rich Dad series, Kiyosaki writes with the authority of someone who has spent decades teaching people to think differently about income and independence.

More by Robert T. Kiyosaki

Why "A" Students Work for "C" Students and "B" Students Work for the Government: Rich Dad's Guide to Financial Education for Parents

Robert T. Kiyosaki

Rich Dad's Who Took My Money?: Why Slow Investors Lose and Fast Money Wins!

Robert T. Kiyosaki

Rich Dad's Cashflow Quadrant: Rich Dad's Guide to Financial Freedom

Robert T. Kiyosaki

Rich Dad's Guide to Investing: What the Rich Invest in, That the Poor and the Middle Class Do Not!

Robert T. Kiyosaki

You Might Also Like

Browse by Category

Ready to read Rich Dad’s Cashflow Quadrant: Guide to Financial Freedom?

Get the full summary and 100K+ more books with Fizz Moment.